Finance is the industry with the most to lose from AI getting it wrong. Regulatory accuracy, brand trust, product complexity - when an AI system mischaracterises a financial institution or cites the wrong source for a claim about rates, fees, or risk, the consequences go beyond a missed marketing opportunity. They affect compliance, reputation, and consumer confidence.

Which makes the findings from this benchmark worth examining carefully.

GenSight.AI ran deterministic AI visibility audits across fifteen of the world's largest and most recognisable financial institutions, spanning three groups: Traditional Banking and Financial Services, Digital-First and FinTech, and Insurance, Wealth and Asset Management. The benchmark included JPMorgan, Goldman Sachs, HSBC, BlackRock, American Express, Revolut, Stripe, PayPal, Wise, Robinhood, Fidelity, Vanguard, Allianz, AXA, and Charles Schwab.

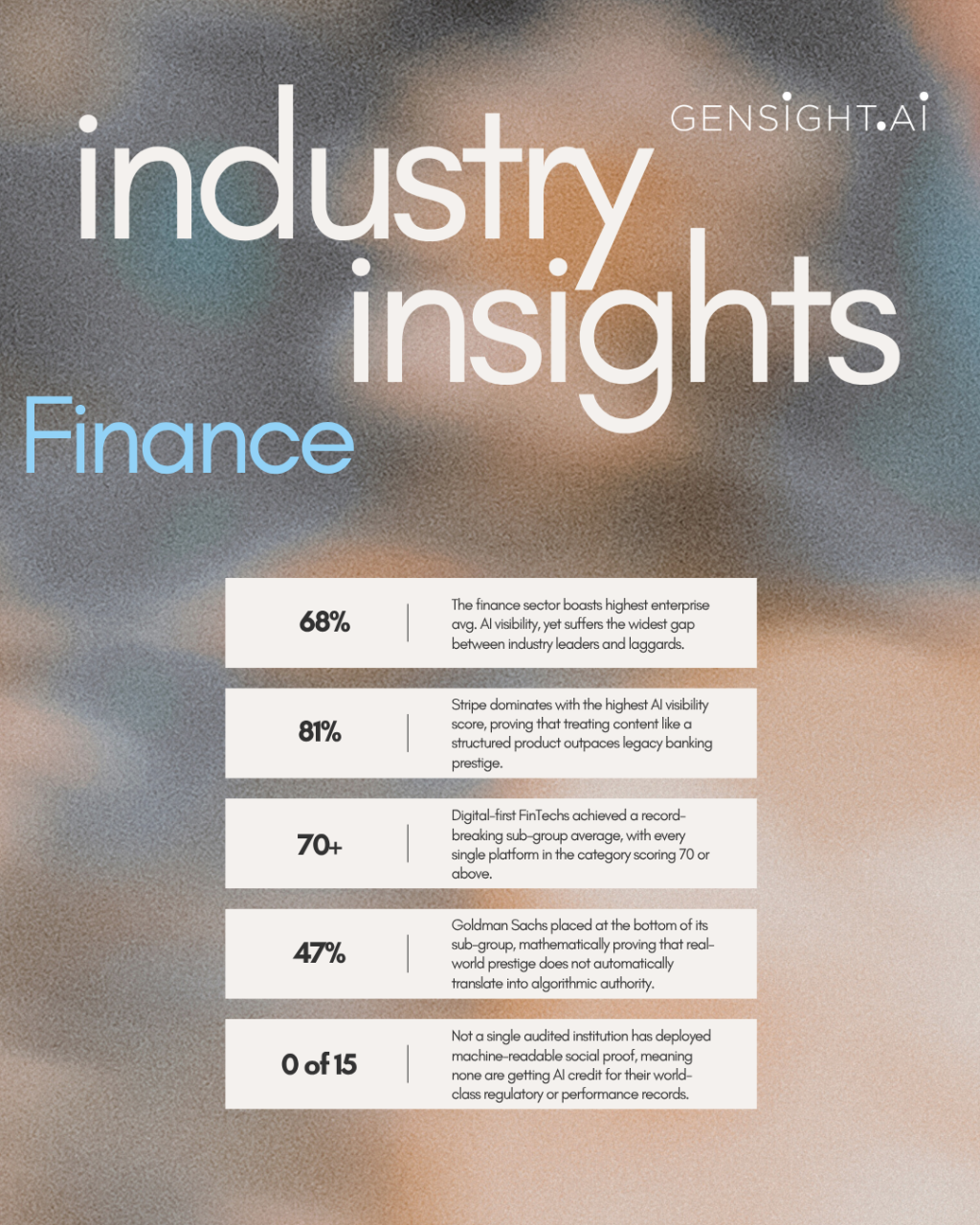

The average AI visibility score across all fifteen: 68 out of 100.

Seven of the fifteen reached the high-performance tier - a score of 70 or above. Eight sat in the moderate band. None scored below 40. On those headline numbers, Finance is the strongest performing enterprise sector GenSight.AI has benchmarked to date, ahead of both Content Marketing platforms and Automotive OEMs. But the range is 34 points wide, and the entity sitting at the bottom of that range is one of the most famous financial institutions in the world.

The Leaderboard

Stripe leads the benchmark at 81 - the highest score recorded across any enterprise benchmark GenSight.AI has run, across any industry. PayPal follows at 73. Allianz sits at 77, Vanguard at 72. At the other end, Goldman Sachs scores 47 and BlackRock scores 64.

The 34-point spread between Stripe and Goldman Sachs is the widest within a single sub-category group in any benchmark to date. Both are globally recognised financial institutions. Both have extensive web presences, significant media coverage, and deep third-party citation networks. The gap is not explained by brand recognition or content volume. It is explained by infrastructure decisions - the structured data signals, entity declarations, and machine-readable architecture that determine how confidently AI systems can place these brands in their competitive landscape and cite them as authoritative sources.

Digital-First Finance Leads the Field - By Design

The Digital-First and FinTech sub-group averages 73 - the highest sub-group average GenSight.AI has recorded across any industry benchmark. Every single platform in this group - Revolut, Stripe, PayPal, Wise, and Robinhood - scored 70 or above. All five are in the high-performance tier.

The explanation for this is structural, not accidental. These companies were built on the assumption that their customers would find them online, evaluate them digitally, and make decisions based on information consumed through screens. Their content infrastructure was designed from the ground up to be clear, direct, and answer-oriented. Developer documentation is structured and API-referenced. Product pages are built around specific, queryable features. Help content is explicitly formatted for extraction.

This is exactly what AI retrieval systems reward. FinTech platforms did not optimise for AI visibility - they optimised for digital-native customer acquisition, and the two things turn out to require very similar infrastructure. The Citation Worthiness average for this sub-group is 71, the highest of any sub-group in this benchmark, and a direct reflection of content that was built to answer specific questions rather than project a brand identity.

Stripe at 81: What the Highest Score in Any Benchmark Reflects

Stripe's score of 81 is the highest GenSight.AI has recorded across Automotive, Content Marketing, and Finance benchmarks combined. Understanding why matters more than the number itself.

Stripe operates as much as a technology infrastructure company as a payments platform. Its developer documentation is among the most comprehensive and machine-readable in the industry. Its content is structured around specific technical questions - how does the API work, what are the fees, how does dispute resolution operate, what are the compliance requirements by jurisdiction. Every one of those content types produces exactly the kind of direct-answer, verifiable, citation-worthy signal that AI retrieval systems use to establish authority.

Stripe also has a strong entity graph - a dense network of independent third-party references, developer community citations, comparison platform presence, and structured data declarations that give AI systems the corroboration they need to cite it confidently rather than hedge with a competitor. Its Retrieval Optimisation score of 68 is the highest in the benchmark, meaning AI can extract and attribute information from its content more efficiently than any other platform audited.

The lesson from Stripe's score is the same as the lesson from WordPress leading the Content Marketing benchmark: the companies that lead on AI visibility are not the largest or most famous. They are the ones that treated digital infrastructure as a product discipline rather than a marketing function.

Goldman Sachs at 47: The Prestige Brand Problem

Goldman Sachs is the most striking individual result in the Finance enterprise benchmark. By any human measure of financial authority - brand prestige, media coverage, analyst influence, global institutional presence - Goldman Sachs is among the most recognisable financial organisations in the world. It scored 47.

That score does not mean AI systems do not know who Goldman Sachs is. Source Eligibility - the measure of whether a brand is considered eligible for citation at all - is high. The problem is what happens between eligibility and citation. Entity Strength is below the sub-group average. Retrieval Optimisation is the lowest in the Traditional Banking group at 55. Organisation Schema is absent. llms.txt has not been deployed.

Goldman Sachs produces enormous volumes of high-quality research, market analysis, and economic commentary. Most of it is published in formats optimised for institutional readers rather than for machine retrieval: PDFs, gated reports, email distributions, and press release formats that are poorly structured for AI extraction. The content exists. The infrastructure that makes it citable by AI does not, in most cases.

This is the prestige brand problem at its most extreme: a company whose authority in the human world is essentially unquestioned, but whose AI visibility infrastructure reflects decades of publishing for a different medium entirely. The gap between Goldman's human reputation and its AI visibility score is arguably the most instructive data point in this entire benchmark.

Traditional Banking Lags - and the Regulatory Irony

The Traditional Banking and Financial Services sub-group averages 63 - ten points below the FinTech group. JPMorgan scores 66, HSBC 69, American Express 67. These are institutions with some of the largest content operations in financial services, yet their AI visibility consistently lags their digital-native counterparts.

The structural explanation is partly regulatory and partly historical. Traditional banks publish extensively, but a significant portion of their output is regulatory disclosure, legal documentation, and compliance-driven content - formats that are often structured for legal review rather than machine consumption. Their customer-facing content tends toward brand narrative and product marketing rather than the direct-answer, FAQ-formatted, structured-data-rich content that earns AI citation.

There is also an irony embedded in the regulatory dynamic. Financial services firms operate under some of the strictest publishing standards in any industry. They invest heavily in ensuring their content is accurate, compliant, and legally defensible. Yet the same caution that produces rigorous compliance documentation also tends to produce content that is dense, hedged, and structured for human legal review - the opposite of what AI retrieval systems are designed to consume.

The banks that close this gap will be the ones that find a way to produce structured, direct-answer content that is both AI-readable and compliant - not an easy challenge, but an increasingly necessary one.

The Universal Gaps

Across all fifteen institutions in the benchmark, several signals are absent with near-universal consistency. Not one has deployed an llms.txt file. Organisation Schema is missing from most of the group. Structured, machine-readable social proof - aggregate review ratings, verified customer satisfaction scores, structured award and recognition data - is absent across the entire benchmark without exception.

In financial services, this last gap is particularly consequential. When a consumer asks an AI system which bank has the strongest customer satisfaction ratings, which wealth management firm has the best long-term performance record, or which payments platform has the lowest cross-border fees - the answer is being shaped by whatever third-party signals happen to be most prominent in the model's training and retrieval data, not by the institutions with the best actual ratings.

Financial institutions have spent significant resources earning third-party validation: regulatory compliance records, independent performance ratings, customer satisfaction surveys, industry awards. Not one of them is formatting that validation in a way that AI systems can consume and cite when answering the questions that increasingly shape consumer financial decisions.

The Structural Conclusion

An average score of 68 makes Finance the strongest enterprise sector benchmarked to date. The FinTech sub-group's average of 73 is the highest sub-group result across all industries. Seven of fifteen institutions in the high tier is a stronger distribution than any other sector.

But the 34-point range, the Goldman Sachs result, and the universal absence of structured social proof tell a different story beneath the headline numbers. Finance is a sector where AI visibility infrastructure is unevenly distributed - concentrated among digital-native platforms that built for the right medium from the start, and significantly weaker among the legacy institutions that carry the most human authority.

As AI becomes a more significant interface for financial decision-making - for consumers researching products, for investors comparing managers, for businesses selecting payment infrastructure - that structural imbalance will compound. The institutions that treat AI visibility as an infrastructure question rather than a content question will define the default answers that AI gives about their category. The ones that do not will watch digital-native competitors fill the gap.

Data derived from the GenSight.AI Industry Benchmark Index by running deterministic vector gap analyses across the top entities. Bulk indexing capabilities will be available to partners on the Agency tier.